Peter Drucker famously said, “Culture eats strategy for breakfast”. This is often interpreted as culture being more important than strategy. These might not even be his words, which makes it hard to know his thoughts, but having built a company to almost 500 people, it’s obvious to me that culture isn’t more important than strategy, it is strategy.

I am confident he knew this. He worked with the Japanese manufacturing companies in developing their culture of kaizen, which helped them to dominate the automobile manufacturing world, and their practices have gone on to fundamentally change manufacturing as an industry.

Your strategy is not what you’re trying to do (those are your goals), but rather how you plan to do it, and your culture determines how you work. Pick any great, differentiated strategy, and you’ll see that how it translates the company culture is what determines its efficacy. We tend to think of culture as being about how people feel, or how they treat each other, but that’s a bare shadow of its importance.

Southwest is an amazing airline. In an industry with a long history of losing money, they’ve managed to make money year after year. How? Their strategy is simple: Be the lowest cost carrier. This isn’t something that the management says to the team who then try to interpret it; it shows up in every decision made by everyone in the company. It’s baked into the culture. If it weren’t, costs would creep in at every level of the organization. They could not be the lowest cost carrier without a culture of parsimony at every layer of the company. You will not be a culture fit at Southwest if you can’t be cheap.

Toyota is legendary for helping to drive a revolution in manufacturing, and their success is based on tight integration between company strategy and behavior at the front line. Many of their practices work against human nature, such as their “Five Whys” tactic, which seeks root causes for quality issues by refusing to blame individuals. Their culture is so unique that one of its standout features is how reliant they are on training and mentoring, from the front-line worker to top executives. Managers get promoted based on their ability to train their teams up, not just for driving results. Toyota understands its success is reliant on its management chain to connect company strategy to front-line execution, and it invests accordingly.

Atlassian has built an amazing business, not by being better at selling, but by ensuring the customer can sell themselves. The entire company maintains the cultural discipline of removing barriers to a sale, of asking why a customer needed help, hit a roadblock, or didn’t buy. This sounds easy, but it’s fundamentally hard, and more importantly it’s directly in conflict with the sales culture of modern software companies. You have to choose whether you care more about this deal or all deals, and Atlassian’s rare choice, and how that has permeated their culture, is a big part of why they’ve done so well. I expect Atlassian has lost countless great people who could not make that shift.

These companies demonstrate the inseparability of culture and strategy. Your strategy is how your company plans to win, and your culture is how people individually behave in alignment with it.

Some might argue that the above are the company missions, not their strategies, but they’re very different. Toyota’s mission is to build great cars, and a culture of kaizen is how they do it. Southwest’s mission is probably something like “Enable access to air travel to all”, and being low-cost is how they do that. Atlassian’s mission is clearly around enabling collaboration between teams, which they support by making their products easy to acquire.

If you’ve got competition, then your strategy needs to specify how, exactly, you’ll beat those competitors. You and your competition can have the exact same mission, but by definition your strategy needs to be different from theirs - you both have the same goal of taking the market, but you necessarily will be approaching it differently. If you don’t have competition, your strategy needs to clarify how you’ll win in a market where no one has thrived before. Neither of these is a simple question of setting goals; it’s about clearly stating how you’ll accomplish them.

Too often, strategies are placed on a pedestal, gesticulated at from afar and never allowed to get dirty, when a strategy’s value is entirely determined by how it hits the ground. Napoleon was one of history’s best military strategists, and he knew the importance of how it translated to individual soldiers. When he gave orders, he demanded they be repeated back word for word, and would do it again until they were right. He knew a strategy’s value was determined where it met the enemy, not when it was laid out in the command tent.

Contrary to what you might hear, I don’t think I’ve ever met a founder who didn’t have a strategy, and usually a pretty good one. In contrast, I have yet to meet an early-stage founder who can explain how that strategy will translate on the ground, or who invested hours every week in ensuring that his or her team was operating according to it. Even basic things like having better usability are hand-wavy at best, relying on constant input from founders rather than permeating the organization’s culture.

Simon Sinek has helped lead the charge in the value of ‘why’ as a force for motivation and alignment. Your strategy for how you plan to win is just as important, and is much harder to align a team around because it necessarily involves daily discipline. It’s not enough to have a great strategy or a great culture; they have to be one and the same.

Your culture is how your strategy is executed, and you’ve got to put in the time to make it work.

Software has the potential to increase productivity as much as electrification or steam power did, but its impact is stunted by its reliance on random interactions. Part 6 of a series.

The venture capital ecosystem bills itself as a meritocratic miasma of genius, with smart founders getting smart money from smart investors. In reality, there is an overwhelming reliance on privileged people bumping into each other at just the right time. This serendipity has spawned some great companies:

Warby Parker was started because someone in an elite graduate program lost an expensive pair of glasses.

Apple was started by a couple of guys who met at a hobbyist group in the computer heartland.

Google’s founders met when one of them gave a tour to the other when he arrived at Stanford for a CS graduate program.

But how many great problems are being ignored because we didn’t get that lucky alignment of particles?

The remodeling industry is a perfect example. It’s an 83 billion dollar market, yet it’s only now starting to see software solutions. The industry itself bemoans neglect by the software industry. The article linked above has some impressive stats about how much waste they experience:

“…studies suggest 30 percent of the construction process is re-work, 60 percent of labor is wasted, and only ten percent of losses are due to wasted materials”

Shouldn’t there be companies fighting tooth and nail over that market? Shouldn’t there be tons of solutions out there, spending money like Uber and Blue Apron are to acquire new customers and take a cut of the productivity gains?

Yet I’m in the late-stages of having a garage built at my house, and as far as I can tell software was only used during design, not actual production. One of the contractors we considered seemed to be an Excel wiz, but wasn’t using off-the-shelf software. How many months of productivity could have been added back into these teams’ lives if they had better tools? How much less disruption could I have experienced, and even, how much less could I have paid if my contractor could get three jobs done in this time because she was so much more productive?

(Did you notice that even I’m relying on the serendipity of my building a garage to illustrate my point that VC relies too much on it?)

In a rational world, every reasonably sized market would have a well-funded ecosystem of software companies vying to take it into the information age. When I got my home equity loan for the garage, I should have been inundated with offers from software companies to help improve the project. Heck, someone should have offered me the loan interest-free if only I required my contractor use their software. Instead, my project is late, costs me more, and makes less money for all the workers because it’s left out of the information technology revolution.

And that’s just one industry, chosen at coughrandomcough. What about all of the other industries the software kings have not yet anointed as worthy, filled with deeply skilled and energetic experts who aren’t lucky enough to run in the right circles, or live in the right zip codes?

Venture investors famously want passion for the problem they’re investing in solving, so much so that the companies also then demand that any employees also be passionate in turn. And we want our software companies started by developers, by product people, not by business analysts. Or carpenters.

So now to start a company you’ve got to have a software developer thrilled about and experienced in a problem, able to accept the risks that come with starting a company (e.g., health insurance and wage loss), who is living in or can move to San Francisco, and hopefully is a white dude who went to Harvard or Stanford. One way to look at that is how discriminatory it is, but another way is just how much you’re relying on everything lining up just right. It might be that you’ll find a Stanford-educated software developer who deeply cares about building houses and can take the leap into entrepreneurship. But what are the odds that that person has the right insight at the right time, and then can find the right people to partner with?

Twenty years in I’m still awed by the opportunity for software to connect, educate, and empower people, but I’m incredibly disappointed by how little of that opportunity we’re progressing against. I think our inappropriately slow revolution is in large part thanks to this reliance on randomness. We have got to get past this if we truly want to get the most out of software before the heat death of the universe (coming more quickly now with all the power being consumed to mine bitcoin). If we can build an environment that does not use serendipity as a crutch, I am convinced we can generate more great companies, and importantly these companies can cover a broader swathe of the economy, and be run by a more representative sample of the market.

Let’s look to biology to see how much of a difference shifting to a constructed environment can make. Living creatures are full of enzymes, which are basically proteins that speed up the rate of a reaction. These reactions are critical to the function of the organism, and without the enzymes speeding them up, life as we know it could not exist. (Conveniently, I did my senior thesis at Reed College on protein structure, so I’ve got some knowledge here.)

In most cases, the reaction that they catalyze (that is, cause to happen) would happen without the enzyme, but it would do so at a far slower rate. For instance, mammalian milk contains the sugar lactose. This sugar will break down in water into glucose and galactose of its own accord, but not quickly enough to digest all the lactose in milk you drink. Mammals have evolved the enzyme lactase, which causes this splitting of lactose into simpler sugars to happen much faster.

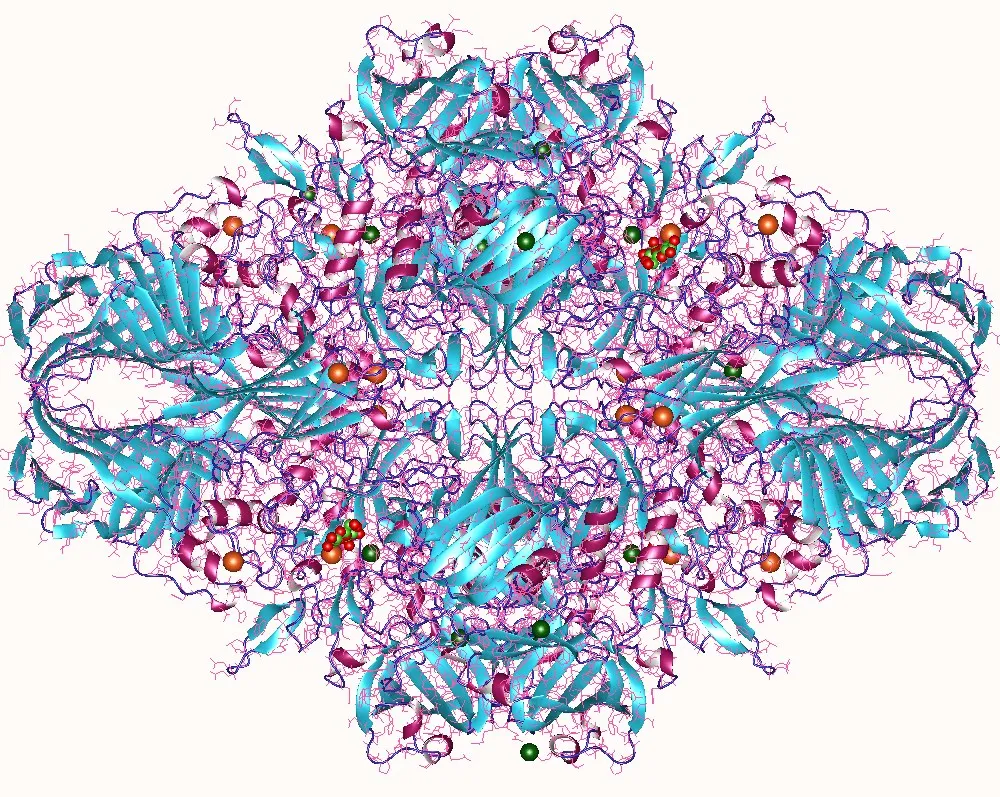

Enzymes are incredibly complex — lactase has 1927 amino acids in five separate groups, arranged in an amazing 3D structure:

A rendering of the structure of lactase

This huge structure is all necessary to enable the protein to place a lactose molecule near a water molecule in exactly the right arrangement to ensure the reaction happens immediately, every time, instead of eventually, sometimes. For all this structure, the site where the reaction takes place is quite small, just big enough for the two target molecules. Those 1927 amino acids mean the protein is about 37,000 atoms. Lactose is 35 atoms, and water is, ah, 3.

That’s a lot like designing a building the size of a sports stadium just to catalyze a meeting of two people.

How much quicker does the enzyme work? About 75% the world’s human population is lactose intolerant, meaning that if they drink milk as an adult, the lactose will cause adverse reactions instead of safely being broken down in the intestines. The rest express enough lactase that they are able to comfortably metabolize lactose, and thus can drink as much milk as they want. Again, remember that lactose breaks down in water on its own, just too slowly to be useful.

So here we have a situation where one of the major sources of calories around the world — cow’s milk — is enabled by this enzyme dramatically speeding up reaction rate.

What does this have to do with venture capital?

Again, venture today is heavily reliant on serendipity; that is, the right people bumping into each other at the right time in the right context. This is exactly how chemical reactions happen normally: Two molecules (e.g., lactose and water) live near each other, and every so often they bump into each other in a way that enables the reaction to happen. Most of the time, however, they fail to hit exactly the right setup, and nothing happens.

When the enzyme is present, though, its unbelievably complex structure ensures that the water and lactose molecules are placed into exactly the right orientation every time, and bam, magic happens.

The probability of a great company getting founded today is a lot like the probability of lactose degrading naturally: It happens, but slowly and infrequently.

I smile at the idea of complexes the size of sports stadiums built for speed-dating founding teams, but that’s not necessarily what I’m recommending here (although if that’s your plan, I’d love to consult on the project).

Even if we wanted to, I don’t think we could build a structure (physical or otherwise) like this, because we don’t yet understand yet what it takes to build a great software company, which means we can’t construct or evolve a perfect environment in which to make it happen.

All I really know is that what we’re doing now isn’t working. We’re not attacking the right markets, we’re not including enough people, and we’re not having a big enough impact on the economy.

For our ecosystem to be healthy, for it to be effective at transforming the industries that need it most, it has to do something differently. We can really only increase the rate of great company creation by increasing the rate of experimentation, or increasing the rate of success. Incubators and early stage investors are doing what they can to run more attempts in parallel, somewhat like a generative algorithm, but this is bound to have little impact because the goals — “be worth a billion dollars” — are so separate from the founding event. Investors are starting to figure this out and pull efforts back accordingly.

That leaves us the challenge of finding ways to increase the rate of success.

Of course, I have my own ideas for doing so, but I was always told as a leader my job was to present the challenge to the team and leave the problem of solving it to them.

Venture capital’s reliance on unicorns provides cover for the huge failure rate of startups, and investors make no effort to reduce it. Part 5 of a series

Venture investing is fundamentally uncertain. You’re making big bets on people, ideas, and markets that might never work out, and there are more ways to fail than succeed. As a result, investing has to take into account the likely failure of many efforts. If your financial model assumes each of your investments will be a success, you will have a short career indeed.

Manyinvestors have written about how they need some companies to win big in order to cover for other companies failing completely. As a simple example, Fred Wilson at Union Square Ventures tells his investors to expect 1/3 of his investments to fail, 1/3 to return their capital (which is also failure; they sell for a small enough amount that investors just get their money back, and in most cases the founders and employees get nothing), and 1/3 to “succeed”, where his definition of success is that they return 5-10x the original investment.

He says his actual record is a bit better than that, but like Warren Buffet, he’d apparently rather set achievable expectations.

Let’s use some concrete examples. Remembering that most companies raise more than three rounds of funding, and keeping in mind that investors usually get about 20% of your company through each of those first few rounds, here’s what needs to happen to deliver that 10x return:

Your seed round is $500k at a $2.5m pre-money valuation, so you have to sell for $25m dollars. The investor gets $5m, and founders split $20m.

Your A round is $5m at a $25m pre-money valuation. Now your company has to sell for $250m. Each investor gets $50m, and the founders split $150m.

Your B round is $15m at a $75m valuation. Your target exit price is now almost $750m. By this time the founders own less than 50% of the company, but hey, if you can exit at that price everyone is pretty happy. Notice also that while this is a solid 10x win for the last investor here, it’s delivering close to a 300x return for the first investors (not counting pro rata costs). It’s nice work if you can get it.

Beyond three rounds, investors usually have smaller return expectations (e.g., 3-5x) but also have a shorter time horizon. That growth round investment of $50m is only expected to turn into $150m or so, but it needs to do it in 3-5 years instead of 7-10. Tripling a $750m valuation ends up being pretty hard in any time horizon.

It’s worth noting that if the company sells for $20m after that B round, then the founders get nothing. According to the preference stack (where the later investors all have priority over earlier ones), even with the cleanest term sheet the B and A investors get all their money back, but the seed investor, founders, and employees get nothing. In practice, the buyer will usually negotiate something for the employees and founders — you rarely buy a company without wanting some kind of golden handcuffs on the people who work there — but it’s basically a pittance. You’ve always got to manage your downside, even while you build toward the upside.

Note how quickly the exit price for the company escalates as you raise money. Realistically, it’s only once you’re around a billion dollars in valuation that you can consider going public, so if you’re smaller than that your only choice is to sell the company.

This model helps to explain the industry fetish for unicorns. The returns you get from a billion dollar exit swamp all the failures. And if those unicorns hide a lot of ills, the really big ones overwhelm even the successes. WhatsApp returned $3b to Sequoia on around $60m invested for a 50x return, which means every other investment in the portfolio could have failed and they’d have still made a ton of money.

You can see how the unicorns make or break a firm. How does this affect how they treat the rest of their portfolio?

When you know that a small percent of your bets end up mattering, you don’t worry much about any individual one, and that plays out in the world of venture capital.

Obviously investors don’t actually ignore the other firms; after all, they don’t really know which ones will win big. Equally, though, there’s no evidence they care whether any given startup succeeds.

Of course, investors would say otherwise: They’d say they work incredibly hard to help their companies, they work massive hours, answer the phone late at night, etc. Sure. I mean, they don’t put in nearly as many hours as the founders they’re helping, or even as much as a typical financier does (just thinking of the hours bankers put in these days makes me shudder) but I do believe they work hard. I do have a couple of anecdotes that show it’s not as hard as they’d imply, though.

I had one investor tell me that he loved the transition from operator to investor because the lifestyle is so much better. Again, this is from an investor class that publicly derides “lifestyle” businesses that generate cash for its founders but don’t scale massively. When I asked him about the hypocrisy of him working 9-5 but demanding his founders put in crazy hours, he defended it as their needing to lead from the front. Guess that tells you where the investors aren’t.

I also know a great investor who left a top-tier firm because he said he could not spend any more time working three days a week and being paid for five. Pretty honorable, if you ask me.

But mostly, yes, I do think many investors work hard.I just don’t think the work they’re doing helps their companies much.

Let’s walk through a couple of obvious examples.

Given the high probability of failure of a given investment, you’d think that the industry would be great at reducing the risks for their companies and thus increasing the survival rate. Not so much. For example, many investors have told me that the most likely reason for a company to fail is the team. Ok. So what do they do to reduce the probability that a founding team will fall apart?

Ah… nothing. No coach for each founder, no coaching plan, not even a packet providing best practices. Nada.

Their explanation for this is pretty simple: Coaches are expensive, and the investor can’t afford to have them on staff because the measly 2% on their $300m fund just can’t support bringing on staff to help founders. They could have the company fund it, but then that’s less money going to build the company.

This is the highest risk to your investment, and you’re literally not willing to spend any money mitigating it? Further, you’re tacitly recommending that your founders also avoid this easy bit of risk mitigation? Huh. Ok.

Investors will also tell you that the most valuable resource at a company is the founder’s time, and he or she needs to be laser-focused on building the business. It’s obvious they don’t actually believe that.

We’ve already established that founders will spend about a quarter of their time fundraising, rather than building the company. You could argue that this is the most valuable use of their time, but that’s only true in the sense that it has to be done and there’s no one else to do it. Most founders suck at fundraising and are tortured by their need to focus on that rather than building their business. Investors do help a little with this, but not so much that it implies the founder’s time actually is a precious resource. There’s a pretty clear sink-or-swim attitude around fundraising, even though success at it has little to do with the ability to build and run a company.

You see this same disregard for the founder’s time when you look at what they end up spending it on.

There’s a vanishingly small part of any business that’s truly innovative — maybe some part of your market definition or your solution itself — and everything else you do is disappointingly similar to what every other founder ends up doing. Great, so investors have figured that out and as part of their investment they deliver a playbook that uses the collective intelligence of their portfolio to help founders avoid having to make all the rookie mistakes, right? Hah! Nope!

The best firms do enable founders to talk and work together, but it’s all ad-hoc, and let’s be honest, that’s pretty minimal help. Every founder is basically doing a random walk around the possible solution space for “how to build a great company”, taking on huge technical risk with untried platforms and experimenting with idiocy like holacracy rather than focusing on the most important parts of their business, the one or two bets that will make or break the whole thing.

It shows how little investors are willing to do to help founders mitigate the biggest risks in their business, thus improving its probability of survival. If they cared about their portfolio companies making it, they’d specialize in helping them navigate the different phases of the company, minimizing probability of failure at each phase and especially when transitioning.

So now we see that it’s not just that investors are focused on unicorns, but also that the failure rate that those unicorns cover for is just irrelevant to investors. They know most of you will fail (again, they expect 2/3 to at best return their capital, which is failure in their model and even then only accomplished by a fire sale of the company). Heck, if you don’t fail and instead just continue on being neither a big sale nor a failure, they’ll have to push you into one or the other category in order to close their fund.

As I found running a growth company, success hides many ills. One of the biggest problems in venture capital is how much they let the success of their unicorns hide their indifference to the rest of their companies. This fails their founders, their employees, and the whole market, for no reason other than that it’s easier this way.

I’m convinced that a firm that directly invested in reducing its failure rate would have as many unicorns, but would also have more positive returns throughout their portfolio, and in the midst of building more companies and making more money, they just might do a little good at the same time. That would be a nice change.

The success of companies and founders in modern venture-backed startups is highly reliant on peer validation of investor decisions. Part 4 in a series.

Say you’re an entrepreneur building something new and different, and you know you need capital. After pitching up and down Sand Hill Road (and all over South Park), you’ve finally found a believer, someone who sees what you’re trying to do and thinks you and your team are the ones to do it. Great! Now you can focus on building your business, right?

Nope. Get used to more of the same. You probably raised just enough to get to your next milestone, not enough to get to self-sustaining profitability, which means you’ll be raising again soon. After all, on average startups raise more than three rounds of funding. I know what you’re thinking: But this investor is a true believer, and given how hard it was to convince others, they’ll sign up for the next round instead.

Nope. It does happen, but it’s rare. In general, every round you raise has to be led by a new investor. Part of this is about dollars: Your seed-stage investor writes $500k checks out of a $50m fund, but your A-round investor writes $5-10m checks out of a $300m fund. That seed investor will participate in the larger round (doing what’s called their pro rata, to keep their ownership share the same), but if they led the round they’d burn through their fund too quickly and would not be able to lead enough investments to make their model work.

Even if dollars aren’t the restriction on your first investor leading later rounds, you’ll still likely find yourself pounding the pavement again. Imagine you’re an investor, and you see a peer investor leads follow-on rounds for most of their portfolio companies. One of those companies comes knocking on your door asking you to invest, and of course your natural question is: Why isn’t your existing investor leading? There’s no good answer to that question.

You can’t say, “Well, they’re a bad investor, and I really need new blood”, for pretty obvious reasons. Even if it’s true, badmouthing existing investors will never get you new ones. You can’t say, “Well, they like us, but even though they lead follow-on rounds in 90% of their companies, they don’t like us enough to lead one for us.” You’ve just told this new investor that you’re in the bottom 10% of your investor’s portfolio. Now there’s no chance they’re going to invest. If the investor that knows you really really well doesn’t want to write a check, no one else will.

To prevent this problem, the industry has the habit of not leading follow-on rounds. Again, not that it never happens, but it can’t be the common pattern, because the company that breaks it gets a black mark. I’ve had many investors (including those invested in Puppet, the company I founded) tell me they follow this habit religiously, for exactly this reason. “Nope, as much as I like you, you’re going to have to get the money from someone else.”

Out you go.

Thankfully, venture investors recognize the downsides of this and build deep networks of firms and individuals who frequently work together. There are even later-stage firms who specialize in following specific investors whose track record they trust. But while this pattern was developed for good reasons, it also has downsides that no amount of networking or help can compensate for.

First, of course, it means most CEOs spend a huge percentage of their time either directly raising money or doing the work necessary to do so later. You might not have wanted to become best friends with tens of investors, but if you’re taking venture capital, that’s your job now. Given that investors are professional meeting-takers, they’ve got time to meet for coffee any time, so this can be hugely time consuming. Then when it comes time to actually raise a round, you should expect it to consume your life for at least three months. And that’s the success case.

This time sink is pretty bad if you live near all the investors you need to meet, but what if it’s a flight to the bay area instead of just a drive? Oh, if you’re one of the top companies they’ll come to you, but if you’re not, it’s one more way you have to work harder than the ones they love. It was only in our late-stage rounds we had luck getting investors to come to us, and we were only in Portland, an hour and a half flight away. I can’t imagine trying to raise money in a place that shudder needs a connecting flight to get to. I nearly killed myself in a rented PT Cruiser (the first available car at SFO) trying not to be late to an investor meeting, and of course, he passed on us anyway because I could not convince/did not want his buddy to join us as COO.

This all adds up to a massive tax on the companies that do succeed, where CEOs become experts in fundraising rather than experts in building great companies, which is, of course, stupid. But it has a much worse impact on who and what can get funding in the first place.

Again, put yourself in the head of an investor. You look at tens of potential investments a day, and you have far more opportunities than time or money, so you have your pick of what to invest in. On the one hand you’ve got a woman or a person of color pitching a company that sells to markets they deeply understand, maybe something more focused on customers who look like them. On the other hand, you’ve got a Harvard-educated CS grad who’s found another great use for AI in the cloud.

What we want is for the decision to be made based on what’s the best investment, who’s the best founder, but it’s not. It’s obviously not. If it were, you wouldn’t see such rank discrimination in the world of VC, where women and people of color are almost entirely excluded.

Instead, a key factor is whether the investor believes this person can raise another round. Note: It’s not whether the person actually can, because you don’t know that until you try it. It’s whether the investor thinks they can. And, of course, investors know that women and people of color don’t fit into the pattern of other investors, so they pre-discriminate in expectation that later investors would have anyway. I mean, why give someone $500k if the company won’t be able to raise another round anyway? You’ll lose all your money.

Like with all patterns, it’s as much about the company as it is about the founder. It’s not just about who gets money, it’s about what kinds of problems are worth solving, and what kinds of customers make good markets.

Silicon Valley has a well-known fondness for investing in products that solve the needs of white boys who just got out of college and are having to learn to live on their own, but less obvious is that this means they often consider other customers to be worthless. It is fantastically hard to convince an investor to back a product built for women, or people of color, or international buyers, when the investor is none of those things.

That is, it’s not just about investing in people who are different — it’s that their ideas are different, the problems they care about are different, and the markets they want to attack are different.

In a world where you’re taking risks, where you’re actually focused on brilliant founders in big markets, those differences would be positives, they’d be signs you can do something ground-breaking. But when that world requires multiple rounds of belief, where failure at any round destroys your company, suddenly those differences become reasons for people to say no, for companies not to get funding, for founders not to get support.

There are some firms out there, like K9 Ventures, who make these bets anyway and recognize that it turns their job into finding follow-on rounds for existing investments rather than just finding new companies. Too many investors either don’t see the consequences of this pattern, or preemptively admit defeat and just don’t even consider investing in a company that they are concerned couldn’t get another round.

Once again we see how a key aspect of venture, one that exists for good reasons, has pernicious consequences that help to explain how the world of venture works today, in all its glory and misery.

There’s no obvious fix to the problem, as either an investor or an entrepreneur, if you truly do need capital to grow but you don’t fit the pattern. One of your best defenses is to focus on profitability first, so you don’t need those follow on rounds and the levels of approval required to make them happen, but that’s not possible for every firm, and even when it is it can result in heavy compromises on growth.

Thankfully, there are now firms out there focusing on founders who are women and people of color. These firms will help in multiple ways. First, of course, they’ll provide the direct funding that is not currently available to so many great founders and companies, but second, they’ll begin to build out those networks of social proof that will enable these companies to get as many rounds as they need, rather than just the ones they can provide.

We’re going to need a lot more firms like that to truly unlock the potential of venture capital, to bring world-changing solutions to those who can get the most benefit, wherever they are and whoever they are. I’m hopeful that the competition these new firms bring will change the behavior, and the opportunity, of the existing ones enough to make the difference, but what’s really going to shift behavior is when the companies invested in by these companies start to deliver outsized returns specifically because they don’t fit the pattern.

Modern venture capital is obviously successful, as demonstrated by the fact that five of the world’s six largest companies were funded by it. However, success is as much about what you say ‘no’ to as what you say ‘yes’ to, and venture capital is no different. In addition to delivering massive collateral damage in the course of its work, the current model rejects all ideas that do not fit within its narrow definition of suitable.

The primary contributor to this wholesale rejection is how VC delivers returns, so to understand why it’s broken we must understand how it works. In this article we’ll go deep on how VCs get their money, how they turn that into more money, and what that all means in terms of what ideas they can and will back. Note that we’re focusing here on the ideas not the people; the structural biases against women and people of color will be discussed in later essays (but it’s worth recognizing that they’re just as baked into the model). Ross Beard’s The Innovation Blind Spot goes into great detail on this topic.

Venture capital firms generally have managers and limited partners; the managers are the people we think of as the investors (they sign the checks), and the limited partners are the investors in the firms; they’re “limited” in the sense that they have ownership but no real control. They don’t actually invest in firms; they invest in an individual fund, and all of the roles are built around the fund, not the firm. This is partially why you might seen an investor leave a firm but stay involved in investments from the old firm: the investor is still on that fund even if they’re not at the firm.

Most limited partners are very large financial institutions, like CalPERS, and they work with venture capital as part of a diversified investment strategy. They have pockets of money in all kinds of places, and VC is added in to ensure they have some high risk/high reward investments. These don’t necessarily even deliver better returns (and in general, VC as an asset class does not do that well), it’s there to get the right mix of risk in the portfolio. In most cases, the LPs are represented by people who would not fit in at a venture firm, because they’re usually finance people at governmental institutions.

A fund is raised by investors (“managing partners”, in this context) seeking money from high net worth individuals, institutions, and anyone else with a lot of money lying around. Money is committed for the life of the fund; except in rare cases there is only one way for an investor to get the money back.

One of the strange things about these funds is not just that they are planned to be locked into a fund for a long time, but it can be awkward if they aren’t. Limited partners invest with VCs as a means of putting money to work over something like a ten year period. If the money all gets returned quickly because of an exit, it throws off the spreadsheets and they quickly have to find somewhere else to put the money. This sounds silly, but it does have a real impact.

Venture capitalists then take this money, and use it to buy stock from startups. So now, the fund holds a bunch of stock instead of a bunch of money. Crucially, this stock is all in private companies, which means it’s generally illiquid (i.e., you can’t easily exchange it for cash). It’s also usually preferred stock, which means the investors get a few extra terms around control and how cash is distributed if there’s a below-value exit.

If this were a normal fund, there would be plenty of ways to make money, and the investors could deliver returns however they wanted; they could rely on growth, dividends, sales, or anything else. However, VC funds are limited partnerships with strict rules about what can be done with the money. No matter where you are in a fund cycle, if a company gets sold for cash, you have to distribute that cash to your investors (keeping 20% for yourself, of course). You can’t reinvest it in another company. (This is only generally true; firms that don’t have this restriction are called evergreen funds, and are usually funded by a single institution or family.)

This distribution on an exit is the primary mechanism for VCs to return capital to their investors. The other way is for a company to go public. This is a weirder one — it’s discussed as an exit, because it allows investors to return capital to their LPs, but it’s not a sale of the company. The difference is that the stock is now liquid, which means it’s basically equivalent to cash; the VCs give distribute the now-public shares to their LPs, who can now all trade it in for cash whenever they want.

Ironically, distributing shares to LPs is a big risk to the company — if 50% of a company’s stock is owned by investors, and they distribute all of that stock to their LPs the day a company’s lockup period ends, what do you think the LPs would do? Well, they’re not experts in tech, or high growth companies, and more importantly, this stock doesn’t fulfill the same needs as the VC fund did in their asset allocation, so they sell it. Of course. And what happens to a newly public company who finds that 50% of its shares are suddenly sold on the public market? The stock gets hammered, because a huge upsurge in supply means an equivalent drop in price.

That’s why VCs distribute shares over a broader period of time, usually 18-24 months. They have some flexibility in how this is handled so they can protect these newly-public companies.

Ok, now you understand how it all works — how venture capitalists get money, make money, and then give it back to their investors in turn. Why does that matter?

It matters because there are only two ways for a VC-backed startup to be a success for its investors: Go public or get bought. As the CEO of Puppet, I always said any company has four options: Go broke, go public, get bought, or stay private indefinitely. If you take VC money, that last option is off the table.

It’s worth saying again: You take VC, you are committing to getting bought, going public, or going broke.

Crucially, that means that investors must push you into one of those outcomes. The reason they deride private businesses that generate cash isn’t because they’re bad businesses, it’s because they’re structurally incapable of profiting off of them. Their system is limited to valuing sales or IPOs; nothing else can have value to them, because nothing else allows them to make money.

This means that if you’ve got a great company that’s taken some VC but is at real risk of settling into a mere 20% growth rate with a sight to profitability but only making, say, $30m a year, they’re going to push you out of that comfort zone. They have to. They’ll ask you to raise a “growth” round so you can “really scale this thing”, or they’ll try to sell the company. If that doesn’t work, they’ll just fire you and put someone in place who will do it for them. It’s not because they’re evil, it’s because their contracts essentially require it. They can’t return the stock of a private company to their LPs, so what choice do they have?

Now that we understand how investor behavior is driven by how capital is returned to investors, let’s discuss what it means to the technology startup ecosystem as a whole. (There are VCs for things outside of tech, but the asset class was basically invented for technology, and that’s where it is centered.)

If you’re seeking funding for your technology company, you essentially have to promise that you can and will sell your company for an outsized return, or that you can and will take it public. In reality, almost no one invests with the expectation of a sale; they’re all betting on an IPO, recognizing that a sale is a good second option. It doesn’t matter if you can generate a ton of profit; they have no use for that. In fact, it might get awkward if you started distributing dividends.

This has two big consequences. The first, of course, is that companies that don’t have a realistic shot of going public can’t get venture capital. This is a striking constraint, given how much of our economy consists of small, profit-generating businesses that generate jobs and cash locally, whereas the ranks of public companies that distribute returns only to the investment class have been shrinking for decades. The story they’ll tell you is that only those really high-growth companies “need” VC money, but it’s much simpler than that: Their business model doesn’t work if your company doesn’t sell or go public.

Bank loans do ok at providing funding for low-risk actions by mature companies, and VC does well at funding high-risk companies with the chance to be huge, but there’s a huge gap in the middle that struggles to get any funding. (Both of these funding mechanisms in the US also suffer from being overwhelmingly biased toward only funding white men, but that’s a different essay.) Medium-risk companies often do need funding, but can’t get it, which in many cases means the businesses either don’t exist or end up much smaller than they could be.

The second major consequence is that a lot of companies are able to convince themselves, and thus investors, that they could get big enough to go public. Yes, this is sometimes true, but in so many cases it is instead a lie that both parties tell in order to get the funding done. If you love your company, and the only way to keep it alive is to promise to keep growing, you will. You understand the risks, but they’re better than just letting your company die.

In too many cases, this absolute demand for continued growth is exactly what kills companies. They never learn the operating discipline necessary to generate cash (which, in the end, actually still is king), and they get too big to sustain themselves. At some point, the lie gets out, they can’t get more funding, the fundamental unsoundness of their business model becomes clear, and the whole thing deflates.

When you hear a VC say you should focus more on growth than cash, what they’re saying is, you should worry more about my ability to return capital to my investors than your ability to still have a company in a few years. It might be that growth is the right thing to invest in, but it isn’t automatically the right thing, and it’s at least fair to say that the investor is not a neutral party in this recommendation.

So now we see that so much of what we find poisonous in the world of venture capital is actually the result of how returns are distributed to investors. The growth-at-all-costs mentality, the huge amount of dead companies, pushing employees to work to the bone until you get an exit, and much more can be laid at the feet of this simple constraint.

I don’t know if there is an alternative model that will work in the world of high-risk tech startups, but I do know there are plenty of other investment models that are able to deliver returns without introducing this kind of dysfunction. Conglomerates like Berkshire Hathaway are able to own significant chunks — or even the entirety — of companies and deliver great returns whether via growth, dividends, or anything else. This provides them the flexibility to let their portfolio companies choose their own best means of returning capital to investors. Coincidentally, Berkshire Hathaway is the one non-VC-backed company in that list of six largest companies.

This essay series is an attempt to capture what I’m learning as I’m looking for a new way to invest in great startups. I think it’s possible to build an investment model that directly attacks the weaknesses of VC; success in this quest would mean both huge returns for whoever cracks it, but also a sudden increase in new companies with completely different promises and risk profiles.

I’m a tech founder and recovering SysAdmin. I helped found DevOps and grew up in open source. These days I am convalescing from a decade of physical and mental neglect while running Puppet.

Read more

A rendering of the structure of lactase

This huge structure is all necessary to enable the protein to place a lactose molecule near a water molecule in exactly the right arrangement to ensure the reaction happens immediately, every time, instead of eventually, sometimes. For all this structure, the site where the reaction takes place is quite small, just big enough for the two target molecules. Those 1927 amino acids mean the protein is about 37,000 atoms. Lactose is 35 atoms, and water is, ah, 3.

A rendering of the structure of lactase

This huge structure is all necessary to enable the protein to place a lactose molecule near a water molecule in exactly the right arrangement to ensure the reaction happens immediately, every time, instead of eventually, sometimes. For all this structure, the site where the reaction takes place is quite small, just big enough for the two target molecules. Those 1927 amino acids mean the protein is about 37,000 atoms. Lactose is 35 atoms, and water is, ah, 3.